10 Principal of Investing I follow(how to achieve it)

I have compiled my investing learning and paths with an actionable example of how to achieve or work on it

I've compiled my investing insight – the 10 principal of Investing. These principles are the result of years of learning and experience, presented in a way that I hope resonates with you.

This is not something new which I pen down these are something which I learnt on my way to financial freedom.

Whether you're a newbie in the investing game or a seasoned player, consider this video your checklist. If you're just starting out, use it as a guide. If you're a veteran, share your own principals in the comments below.

Let's dive in!

But why do we even need this ? I usually chalk down as answer.

Increased likelihood of success: By following these guidelines, you can increase your chances of achieving your financial goals.

Reduced risk: Diversification and a long-term investment horizon can help to reduce your risk of losses.

Improved decision-making: By understanding your goals and risk tolerance, you can make more informed investment decisions.

Protection from emotional trading: By avoiding making impulsive decisions based on fear or greed, you can protect yourself from emotional trading mistakes.

Improved financial security: By following these principles, you can build a strong financial foundation for your future.

In a nutshell you can increase your chances of success and achieve your financial goals wisely.

Now lets see some of my own personal principals which I always follow:

1: Set Clear Financial Goals

We all dream of a house, an exotic vacation, a fancy car, our child's education, and more. To achieve these dreams, create a clear roadmap with specific goals, timelines, and strategies.

2: Time is Your Ally

Compounding can turn 1 into 10 in 20 years at a 12.2% annual rate. If you want to expedite the process, you'll need higher returns and patience – the magic duo.

3: Build a Solid Foundation

Your portfolio's foundation should consist of well-thought-out asset allocation, periodic rebalancing, and a clear understanding of what to include and avoid.

4: Balance Risk and Return

Smart investing is about playing the odds. Understand market indicators like PE ratio to gauge when to invest heavily and when to ease off.

5: Don't Chase Past Performance

Avoid the temptation to invest based on recent success stories. Instead, focus on creating a well-balanced portfolio tailored to your needs.

6: Steer Clear of Hot Tips

Hot tips may sound tempting, but they often lead to a game of chance. Always conduct your research and remain skeptical of quick fixes.

7: Embrace the Boring

Wealth-building is a slow and steady process. Don't be swayed by flashy but untested investment avenues; stick to proven methods for consistent gains.

8: Be Wary of Debt

While leveraging can amplify gains, it also escalates risks. Be cautious when using debt in your investment journey.

9: Monitor Wisely, Not Obsessively

Frequent portfolio checks can lead to unnecessary emotional stress. Opt for a less emotional approach by checking in periodically rather than daily.

10: Be a Lifelong Learner

In this age of information, continuous learning is key. Stay curious, explore diverse resources, and build a well-rounded understanding of investing.

Now, lets try to understand how to put this into act.

1: Set Clear Financial Goals

We all dream of a house, an exotic vacation, a fancy car, our child's education, and more. To achieve these dreams, create a clear roadmap with specific goals, timelines, and strategies.

Meet Aarav, a 27-year-old software engineer working in Bengaluru. Aarav, inspired by the first pricipal , decides to set clear financial goals.

Aarav's Financial Goals:

Home in the Hometown: Aarav dreams of owning a home in his hometown, Pune, within the next 10 years. The goal is to save ₹50 lakhs for a down payment on a comfortable property.

Spiritual Sojourn: Aarav is keen on undertaking a pilgrimage to Char Dham in the Himalayas. He plans to save ₹1 lakh over the next 3 years to fund this spiritually enriching journey.

Education Nest Egg: Looking ahead, Aarav anticipates potential upskilling or pursuing advanced education. In 15 years, he aims to have ₹5 lakhs set aside for educational pursuits.

Emergency Fund – The Indian Way: Aarav recognizes the importance of financial security, especially in the Indian context. He plans to build an emergency fund equivalent to 6 months' living expenses, targeting ₹2 lakhs within the next 2 years.

Dana for a Cause: Inspired by his cultural values, Aarav wants to allocate a portion of his income for charity, or "dana" as it's traditionally called. Setting aside ₹5,000 annually for charitable giving is an integral part of Aarav's financial plan.

With these clear financial goals tailored to the Indian way of life, Aarav not only charts a course for his financial future but also aligns his savings and investment strategies to meet these specific aspirations. Setting financial goals in this culturally resonant manner provides a holistic approach, considering family values, cultural practices, and individual aspirations.

2: Time is Your Ally

Compounding can turn 1 into 10 in 20 years at a 12.2% annual rate. If you want to expedite the process, you'll need higher returns and patience – the magic duo.

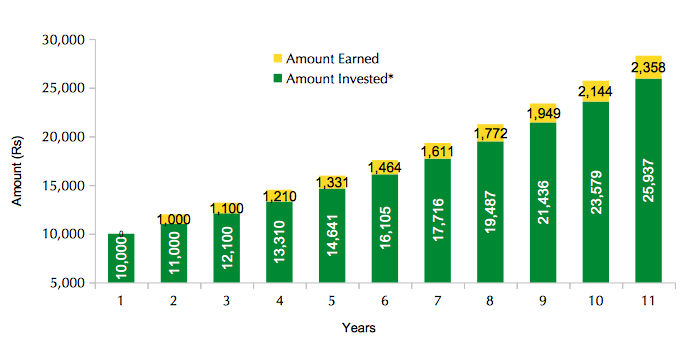

Imagine you invest ₹ 10,000 for 10 years. The rate of interest is 10% per year

At the end of Year 1, you will earn ₹ 1,000/-. Thus your invested amount will grow to ₹ 11,000/-

At the end of Year 2, you will earn ₹ 1,100/-... and so on.

Finally, at the end of year 10, you will earn ₹ 2,358/- for that year, while the initial sum of ₹ 10,000 will grow to around 25,940.

Now, let's explore how Aarav embraces the second commandment: "Time is Your Ally."

Recognizing the power of compounding and the importance of time in wealth creation, Aarav decides to leverage these principles to make his financial goals more achievable.

Aarav's Strategy:

Home Investment: For Aarav's dream home in Pune, he understands that real estate tends to appreciate over the long term. Aarav plans to invest in a mix of equity mutual funds and a dedicated home savings account, allowing his money to grow over the next 10 years. This way, the compounding effect works in his favor, gradually building the necessary corpus for the down payment.

Systematic Investments for Spiritual Sojourn: Aarav decides to start a systematic investment plan (SIP) specifically for his pilgrimage fund. By investing a fixed amount regularly in mutual funds, he takes advantage of rupee cost averaging and the potential for compounding returns over the next 3 years.

Long-Term Portfolio for Education Nest Egg: Aarav acknowledges that education costs may rise over time. To address this, he plans to create a diversified long-term investment portfolio, including equity and debt instruments. By staying invested for 15 years, Aarav allows the power of compounding to significantly grow his education fund.

Emergency Fund with a Growth Component: For the emergency fund, Aarav opts for a combination of a traditional savings account and a liquid mutual fund. This ensures liquidity while also providing the potential for slightly higher returns. Over the next 2 years, the emergency fund benefits from both safety and some growth.

Investing for a Cause: Aarav chooses to invest a portion of his charitable giving fund in socially responsible mutual funds. By doing so, he not only contributes to causes close to his heart but also allows the invested amount to grow over time, making a more substantial impact.

In aligning his investment strategies with the second commandment, Aarav understands that the longer his money stays invested, the greater the potential for compounding returns. By giving his investments time to grow, he optimizes the benefits of compounding, turning time into a powerful ally on his financial journey.

3: Build a Solid Foundation

Your portfolio's foundation should consist of well-thought-out asset allocation, periodic rebalancing, and a clear understanding of what to include and avoid.

Recognizing the importance of a sturdy financial foundation, Aarav takes steps to ensure that his investment portfolio is well-structured and aligned with his goals.

Aarav's Approach to Building a Solid Foundation:

Asset Allocation Reflecting Goals: Aarav carefully allocates his investments based on the nature of his goals. For the down payment on the home, he focuses on a mix of equity and safer debt instruments. His pilgrimage fund and education nest egg also have distinct allocations based on their respective time horizons and risk profiles.

Regular Rebalancing: Aarav understands the need for periodic rebalancing to maintain the desired asset allocation. Every year, he reviews his portfolio and adjusts the weightings to ensure they align with his evolving goals and risk tolerance. This disciplined approach helps him stay on track and manage risk effectively.

Diversification for Stability: Aarav diversifies his investments across different asset classes and sectors to mitigate risks. While he has a portion invested in real estate-linked investments for his home goal, he also diversifies into mutual funds, gold, and fixed-income instruments for stability and balanced growth.

Avoiding Risky Ventures: Aarav steers clear of high-risk ventures, such as investing in highly volatile sectors or individual stocks. He avoids the temptation of quick gains in favor of a more measured and stable approach, in line with his financial foundation.

Selectively Avoiding Certain Instruments: Aarav is cautious about avoiding instruments that may not align with his risk tolerance and long-term goals. For instance, he stays away from investments in high-risk IPOs, keeping his portfolio focused on reliable and time-tested avenues.